Since 1975, tax increment financing (TIF) has been one of Wisconsin’s primary and most successful economic development tools. Statewide, TIF projects have revitalized urban corridors and bolstered industrial growth in Wisconsin’s rural areas. On October 8, the Senate unanimously passed SB 252, which would enhance Wisconsin’s TIF law as the state continues to recover from the Great Recession. The bill will now go to the Assembly for a vote.

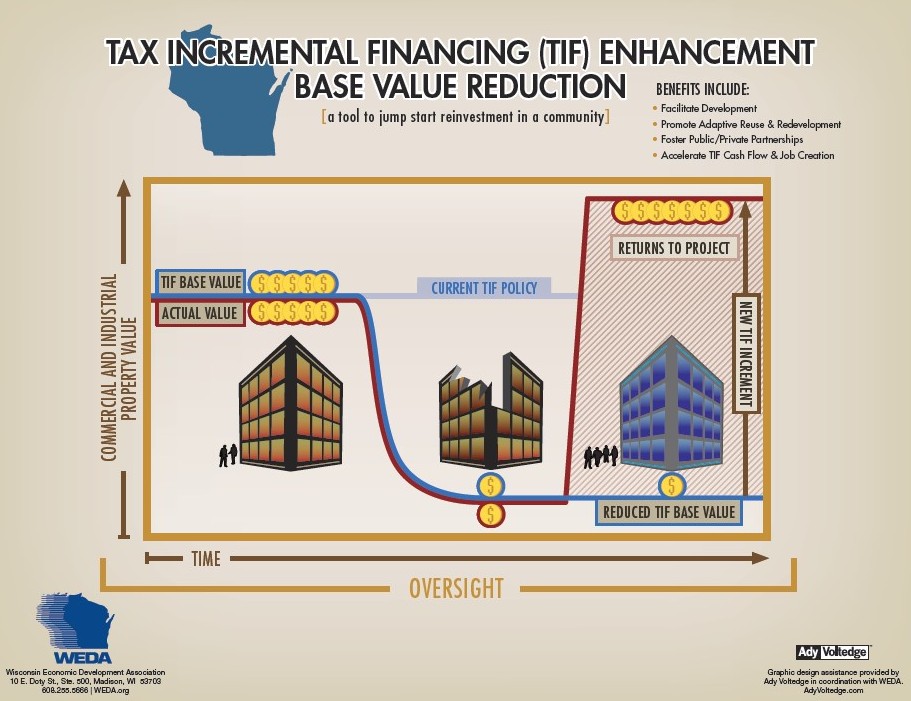

Under current law, when an industrial or commercial property experiences long-term vacancy, when the property has sustained damage from a natural disaster, or when a property has been demolished, the base value of the property in a tax incremental district (TID) remains the same even though the actual or market value may have seriously declined. This discrepancy between the base value and the actual marketplace value, known as decrement, often presents a serious development impediment.

By allowing DOR to reassess a decrement situation within a TIF that has continued for at least two consecutive years, Senate Bill 252 would resolve this issue. The bill defines decrement as a situation where the current aggregate equalized value of all the taxable property within the TIF is at least 10 percent less than the current value of the TIF’s tax incremental base.

By permitting these base value adjustments, communities experiencing this decrement situation can generate positive TIF increment more quickly, increase the number of value-added public-private development partnerships, and accelerate the stream of benefits for all of the impacted taxing jurisdictions (e.g. Local Units of Government, Technical College and School District).